Everything You Had To Find Out About House Mortgages

Created by-Ramirez CarpenterWhen you are buying a new home, it is an exciting time. There is so much to be excited about, but dealing with your home mortgage can be difficult. Finding the best rates and terms is important, as well as paying your mortgage off in a timely manner. Follow the home mortgage tips below to go about your mortgage the right way.

When you get a quote for a home mortgage, make sure that the paperwork does not mention anything about PMI insurance. Sometimes a mortgage requires that you get PMI insurance in order to get a lower rate. However, the cost of the insurance can offset the break you get in the rate. So look over this carefully.

Before you refinance your mortgage, make sure you've got a good reason to do so. Lenders are scrutinizing applications more closely than ever, and if they don't like the reasons you're looking for more money, they may decline your request. Be sure you can accommodate the terms of the new mortgage, and be sure you look responsible with the motivations for the loan.

Getting the right mortgage for your needs is not just a matter of comparing mortgage interest rates. When looking at offers from different lending institutions you must also consider fees, points and closing costs. Compare all of these factors from at least three different lenders before you decide which mortgage is best for you.

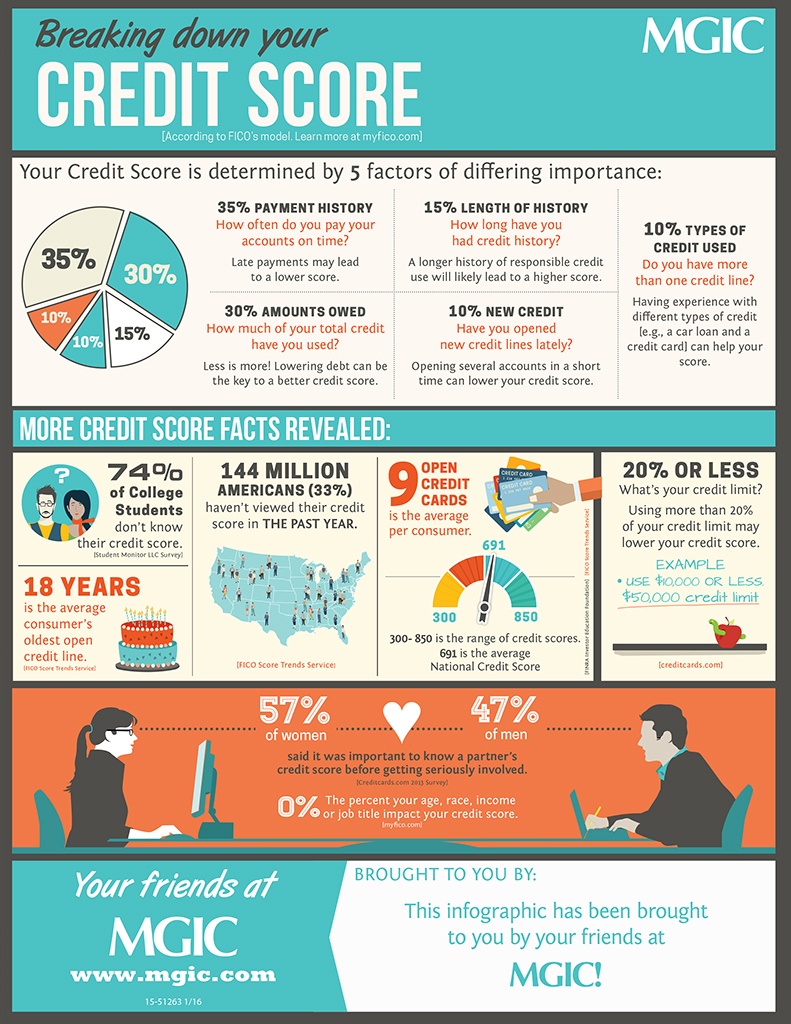

Pay down your debt. You should minimize all other debts when you are pursuing financing on a home. Keep your credit in check, and pay off any credit cards you carry. This will help you to obtain financing more easily. The less debt you have, the more you will have to pay toward your mortgage.

Consider a mortgage broker instead of a bank, especially if you have less than perfect credit. Unlike banks, mortgage brokers have a variety of sources in which to get your loan approved. Additionally, many times mortgage brokers can get you a better interest rate than you can receive from a traditional bank.

Get your documents in order ahead of applying for a new mortgage. All lenders will require certain documents. click over here will be asked for pay stubs, bank statements, tax returns and W2 forms. By gathering these documents before visiting the lender, you can speed up the mortgage process.

Read the fine print of your mortgage contract before signing. Many times home buyers find out too late that their fixed rate loan has a balloon payment tied to the end of the loan contract. By reading over the contract you can ensure that you are protected throughout the entire loan term.

Do a little research on the mortgage lender you may be working with before you sign anything. Don't just trust the word of your lender. Ask family and friends if they are aware of them. Look online. Look up complaints on the BBB website. By knowing as much as possible about the mortgage process, you can possibly save lots of money.

Do not sign a home mortgage contract before you have determined that there is no doubt that you will be able to afford the payments. Just because the bank approves you for a loan does not mean that you could really endure it financially. First do the math so that you know that you will be able to keep the home that you buy.

If your mortgage has you struggling, seek assistance. Think about getting Read Home Page if you are having problems making payments. Counseling agencies are available to you wherever you may live and many are sponsored by HUD. With the help of HUD-approved counselors, you can get free counseling for foreclosure-prevention. Look online or call HUD to find the nearest office.

Avoid paying Lender's Mortgage Insurance (LMI), by giving 20 percent or more down payment when financing a mortgage. If you borrow more than 80 percent of your home's value, the lender will require you to obtain LMI. LMI protects the lender for any default payment on the loan. It is usually a percentage of your loan's value and can be quite expensive.

Set up your mortgage to accept payments bi-weekly instead of monthly. This will let you make more payments every year, greatly reducing the amount of money you spend on interest on the life of the loan. If you are paid biweekly, this is an even better arrangement.

Always be honest during the loan process. If you are not honest, this can cause your loan application to be denied. Your mortgage lender will do the homework and find out the truth.

You need to be prepared to increase your down payment if your credit score is not up to par. A lot of new homeowners save about five percent of the value of their home but it is best to save up to twenty percent. You will be more likely to get a mortgage if you have more saved up for your down payment.

Pay your mortgage down faster to free up money for the future. Pay a little extra each month when you have some extra savings. When you pay the extra each month, make sure to let the bank know the over-payment is for the principal. You do not want them to put it towards the interest.

If you have previously been a renter where maintenance was included in the rent, remember to include it in your budget calculations as a homeowner. A good rule of thumb is to dedicate one, two or even three perecent of the home's market value annually towards maintenance. This should be enough to keep the home up over time.

Ask your lender in advance what documentation they need before you meet with them. This is usually going to include tax returns, income statements and W2s, although more might be needed. The more time you have to get it all together is the less likely you'll be unprepared at the actual meeting time.

As you can see, there's a lot you don't know about the home mortgage business. Using tips like the ones listed above can help you to not only locate a loan but they can also ensure that you find a low-interest loan that won't leave you playing catch-up on a month-to-month basis. So always seek out information before acting.